Last week, the Fed gave markets what they wanted—a second 25 bps rate cut this year—but Chairman Powell’s comments threw cold water on hopes for another in December. Markets wobbled as stocks, rates, and bonds recalibrated. Amid the noise, the giants grew larger: Nvidia, fueled by AI exuberance, became the world’s first $5 trillion company, now accounting for nearly 9% of the S&P 500’s total value. When gains become this concentrated, so does the risk lurking beneath.

A topic that continually haunts all investors is risk. Academics define it as volatility—the fluctuations of asset prices. Others see it as something far more personal: the threat of permanent loss. The two merge when investors turn short-term swings into long-term damage through poor timing.

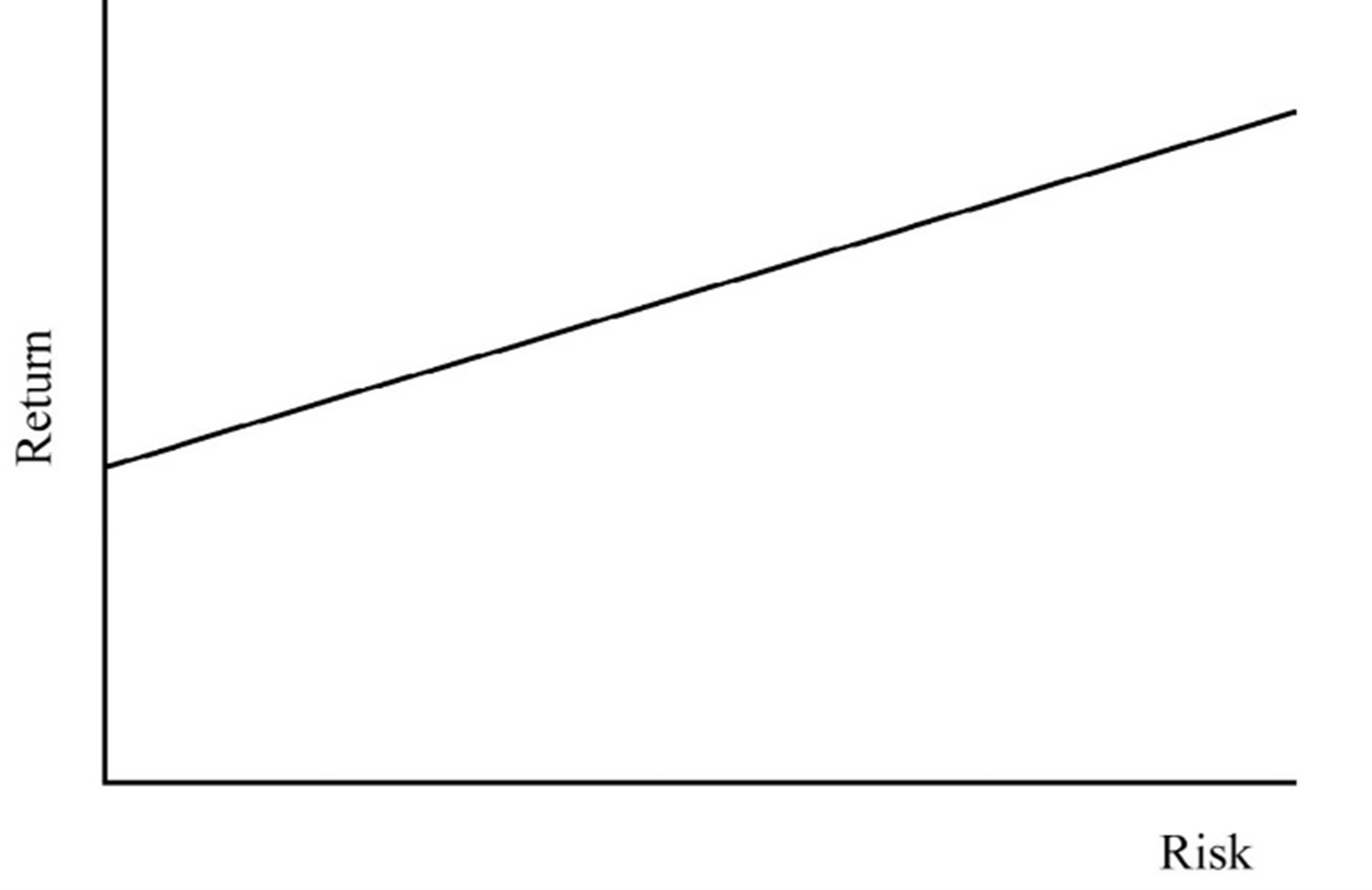

We’re taught that greater risk brings greater reward, but that only holds true if we stay disciplined—resisting panic in downturns and greed during booms. Modern Portfolio Theory distills this into the “Capital Market Line,” a clean visual of risk versus return—simple in theory, problematic in practice.

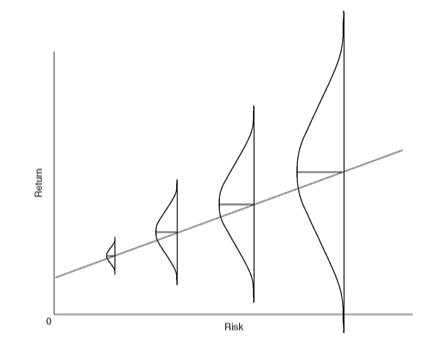

For many (including myself), the Capital Market Line doesn't tell the whole story. Legendary investor Howard Marks filled in the blanks. More risk can lead to greater reward, but the path to higher returns is fraught with jolts, setbacks, and stretches of uneven returns. Jump off at the wrong stop, and even the best-laid plans can derail. That's the beauty of Marks' version—it reminds us that "more risk, more reward" also means "a wider range of outcomes."

The width of your ideal range depends on two factors: your ability and your willingness to carry risk. There's no universal correct answer—only trade-offs. Finding your balance is part science, part art—and it's where Allen Capital Group makes the most meaningful impact on our clients' financial lives.

Being anchored to specific outcomes breeds vulnerability; it becomes poison in times of adversity. The antidote is having a margin of safety: building a plan resilient enough to succeed across many possible futures. Not just the one with low interest rates and perpetually climbing AI stocks.

The financial planning process itself is invaluable, revealing not just numbers but self-awareness. Over time, we realize our needs, wants, and wishes evolve—and that's the point. Flexibility isn’t a flaw in planning; it’s the essence of it. In other words, you must plan on your plan, not to go according to plan.